ISC Accounts Syllabus 2024 has been released by CISCE. If you are studying Accounts in class 11 or 12 in CISCE board, then you can check this ISC Syllabus to know list of topics to refer from ISC Accounts book. This curriculum includes ISC Class 12 Accounts Syllabus PDF, as well as ISC Class 11 Accounts Syllabus PDF. Therefore you should study all chapters given in this Accounts syllabus to be ready for ISC Accounts exams.

ISC Accounts Syllabus 2024

The CISCE syllabus for ISC (Class 12, and 11) is as follows.

ISC Accounts Syllabus 2024 PDF Download Link – Click Here to Download Syllabus

Note that the ISC Syllabus 2023-24 or the ISC 11 syllabus 2023-24 and ISC 12 syllabus 2023-24 are the topics taught during March/April 2023 to March/April 2024 for CISCE exams 2024. Likewise the ISC Syllabus 2024-25 is the list of topics you study from March/April 2024 to March/April 2025 for CISCE board exams 2025. Also that in for some subjects, in certain years, CISCE does not publish class 11/12 curriculum for Accounts separately. In those years it is assumed that the Accounts study topics remain same.

ISC Accounts Syllabus 2024 PDF

The complete course is as follows.

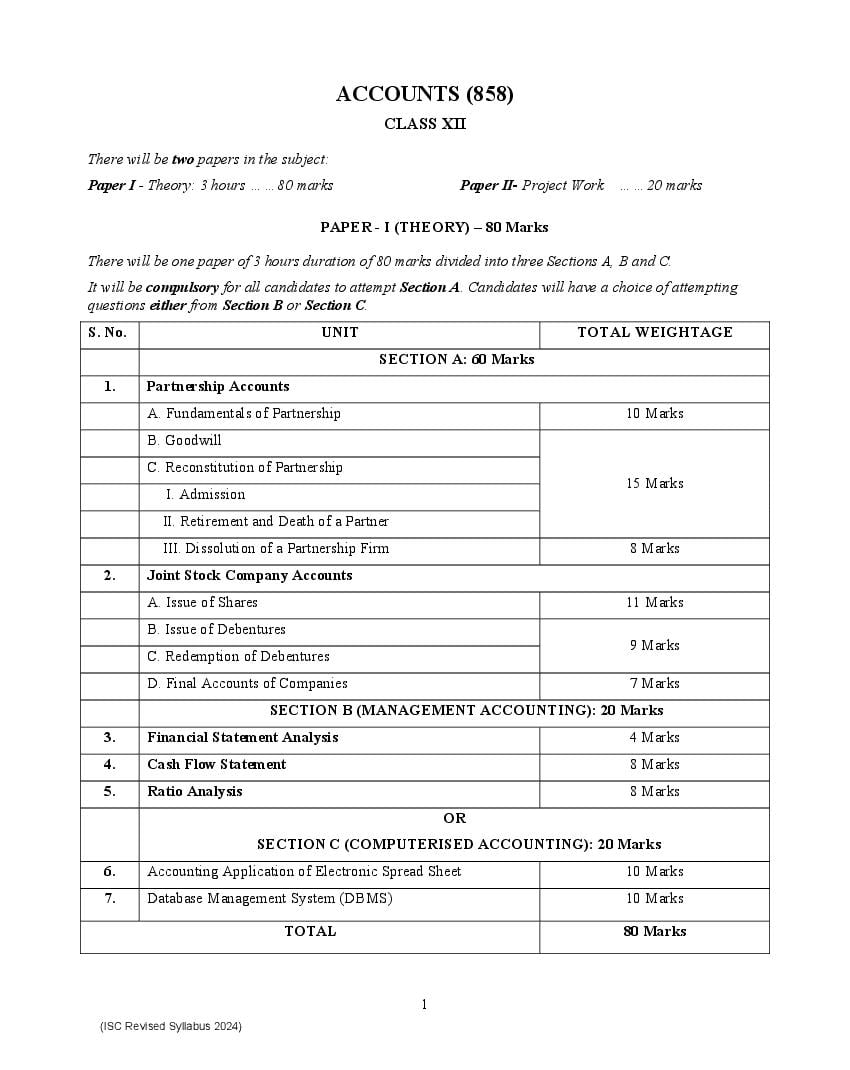

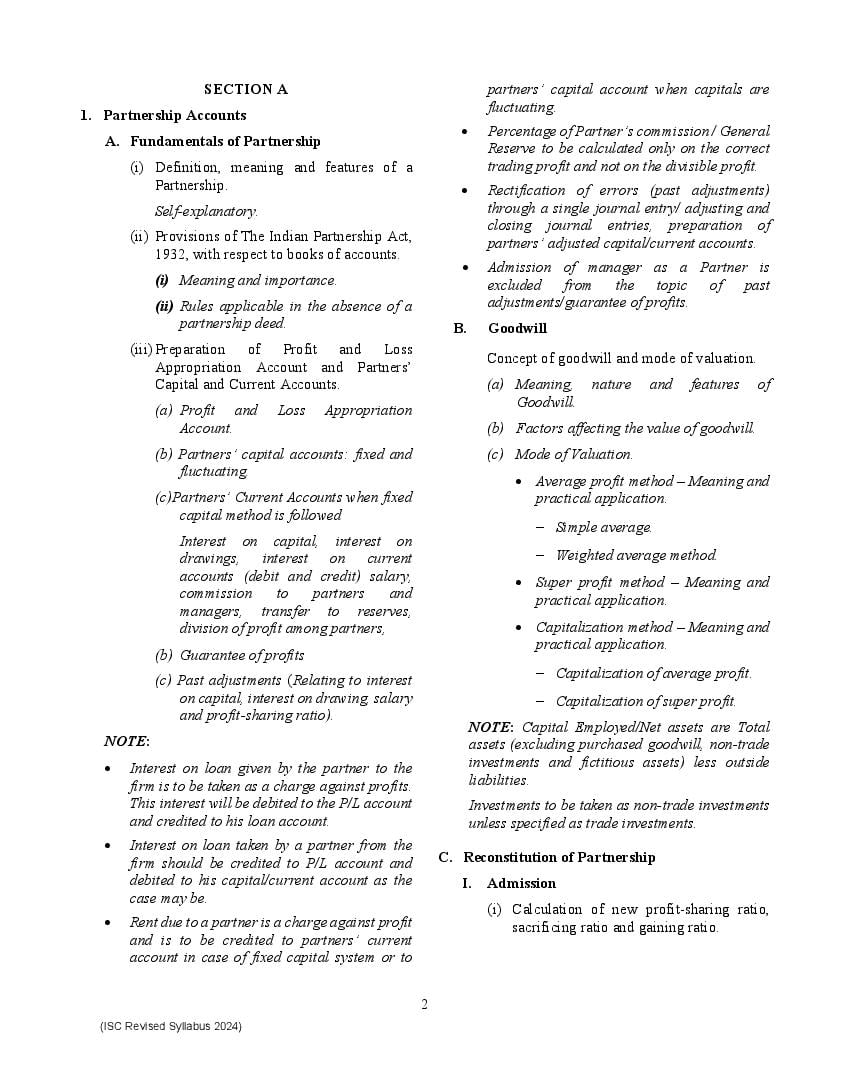

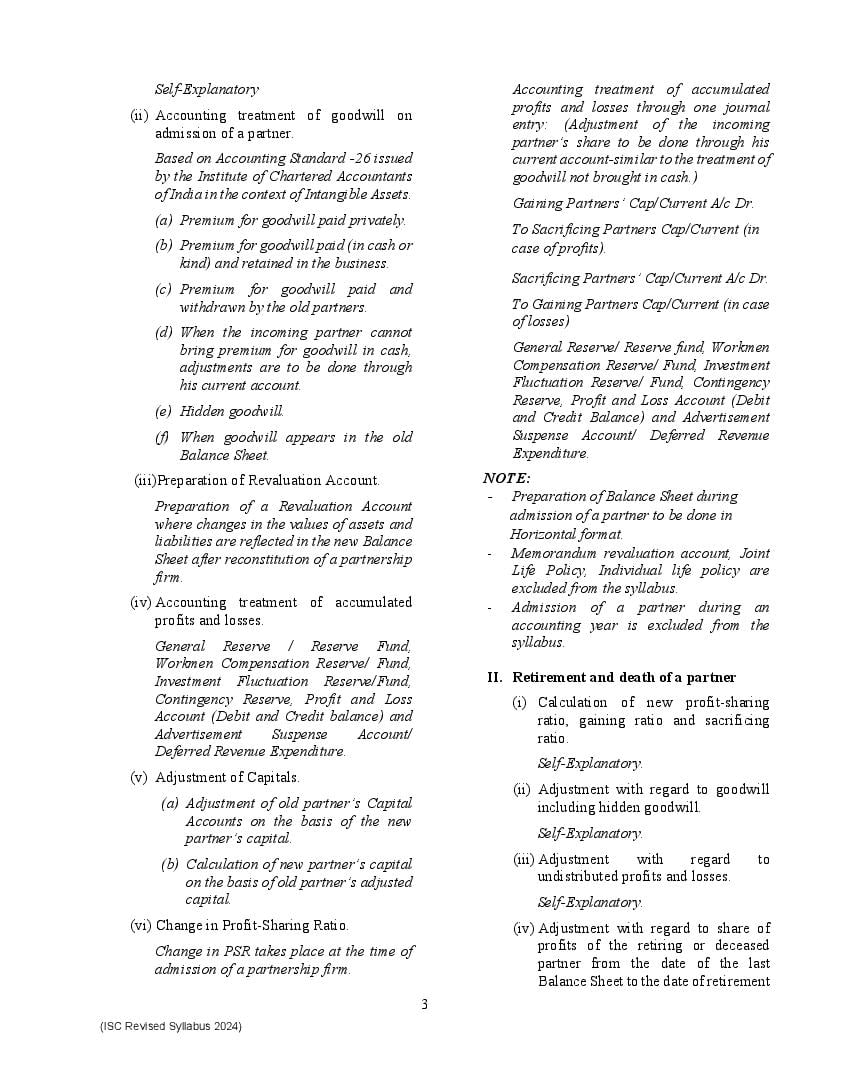

ISC Class 12 Syllabus 2024 Accounts View Download

ISC Syllabus

There are more subjects to study in 11th, and 12th standards in addition to Accounts. So here are the subject-wise curriculum for ISC.

- Accounts

- Art

- Biology

- Biotechnology

- Business Studies

- Chemistry

- Classical Languages

- Commerce

- Computer Science

- Economics

- Electricity & Electronics

- Engineering Science

- English

- English Elective

- Environmental Science

- Fashion Designing

- Geography

- Geometrical & Building Drawing

- Geometrical & Mechanical Drawing

- History

- Home Science

- Hospitality Management

- Indian Languages

- Legal Studies

- Mass Media and Communication

- Mathematics

- Modern Foreign Languages

- Music

- Physical Education

- Physics

- Political Science

- Psychology

- Sociology

- SUPW

CISCE Board Syllabus

Likewise you can check the curriculum for other classes, as follows.

ISC Class 12 Accounts

- If you are in 12th standard in CISCE school, then you need to refer ISC Class 12 Accounts Book to study all topics from syllabus.

- Moreover you can use Selina Solutions for 12 Accounts to overcome difficulties of exercises.

- Then before exam, solve ISC Class 12 Accounts Specimen Paper 2024 and ISC Class 12 Accounts previous year question papers to get an idea of what to expect in exam.

- Also refer Class 12 Accounts notes for CISCE board to revise the topics.

ISC Class 11 Accounts

- Similarly those in 11th standard should study all syllabus topics from ISC Class 11 Accounts Textbook.

- The Selina Solutions for 11 Accounts can be used to solve chapter questions and answers.

- In addition the study material like ISC Class 11 Accounts Specimen Paper 2024, and ISC Class 11 Accounts previous year question papers are critical just before final exams.

- And ultimately Class 11 Accounts notes come in handy for quick revision.

ISC Accounts Syllabus – An Overview

The following are important details about this curriculum.

| Aspects | Details |

|---|---|

| Education Board | CISCE Board |

| Classes | ISC (Class 12, 11) |

| Subject | Accounts |

| ISC Full Form | Indian School Certificate |

| Study Resource Here | CISCE Syllabus for Class 12, 11 Accounts |

| All Curriculum for This Class | CISCE Syllabus for Class 12, 11 |

| Complete Curriculum for This Board | CISCE Syllabus |

| Exam Dates | ISC Time Table |

| Results | ISC Result |

| Previous Year Question Papers | ISC Previous Year Question Papers |

| Class 12 Sample Papers | ISC Class 12 Specimen Papers |

| Class 11 Sample Papers | ISC Class 11 Specimen Papers |

| Official Website for ISC Accounts Syllabus | cisce.org |

If you have any queries on ISC Accounts Syllabus 2024, then please ask in comments below.

To get study material, exam alerts and news, join our Whatsapp Channel.