AP Intermediate 1st Year Commerce Syllabus 2024 contains all the topics you study in Commerce subject in 11th standard. BIEAP (Andhra Pradesh Board of Intermediate Education) issues the AP Inter 1st Year syllabus for Commerce. You can now download the Andhra Pradesh Board class 11 Commerce syllabus PDF from this page on aglasem to know what to study from AP SCERT textbooks.

AP Intermediate 1st Year Commerce Syllabus 2024

The Andhra Pradesh board syllabus for Inter 1st Year Commerce is as follows.

AP Board Intermediate 1st Year Commerce Syllabus 2024 Download Link – Click Here to Download Syllabus PDF

AP Intermediate 1st Year Commerce Syllabus 2024 PDF

The entire curriculum is as follows.

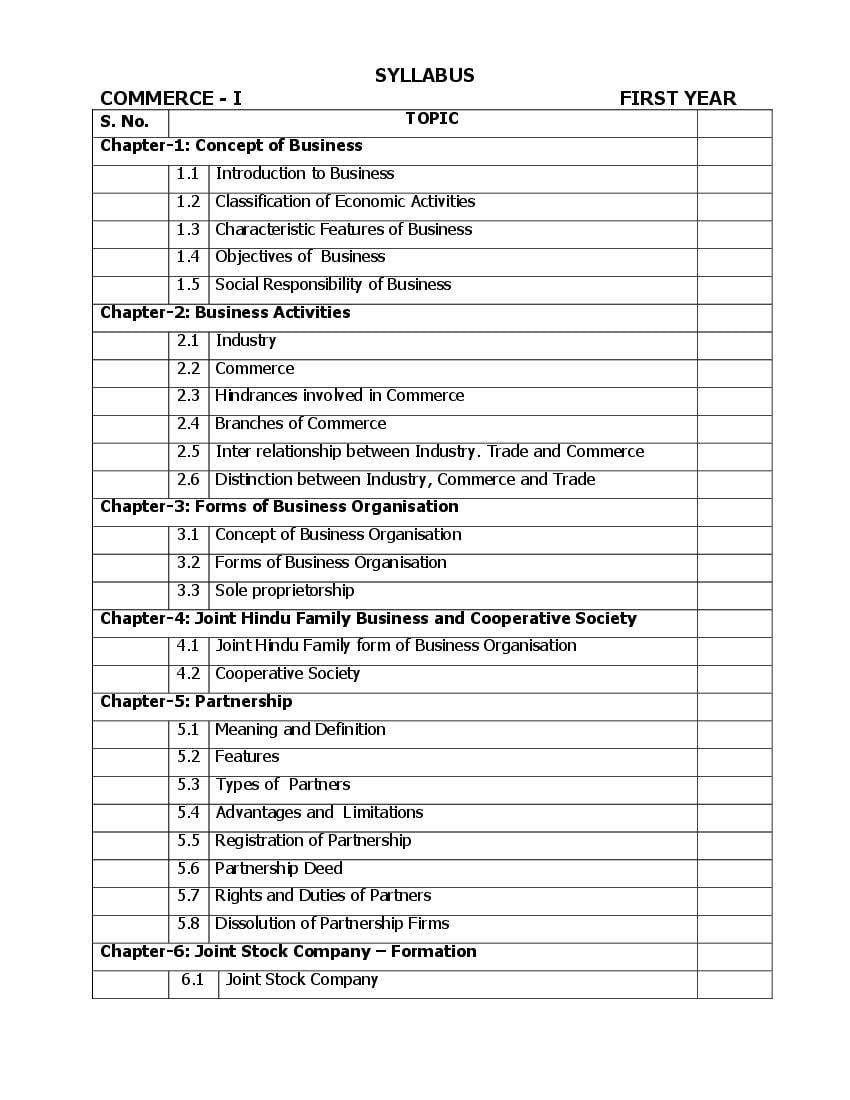

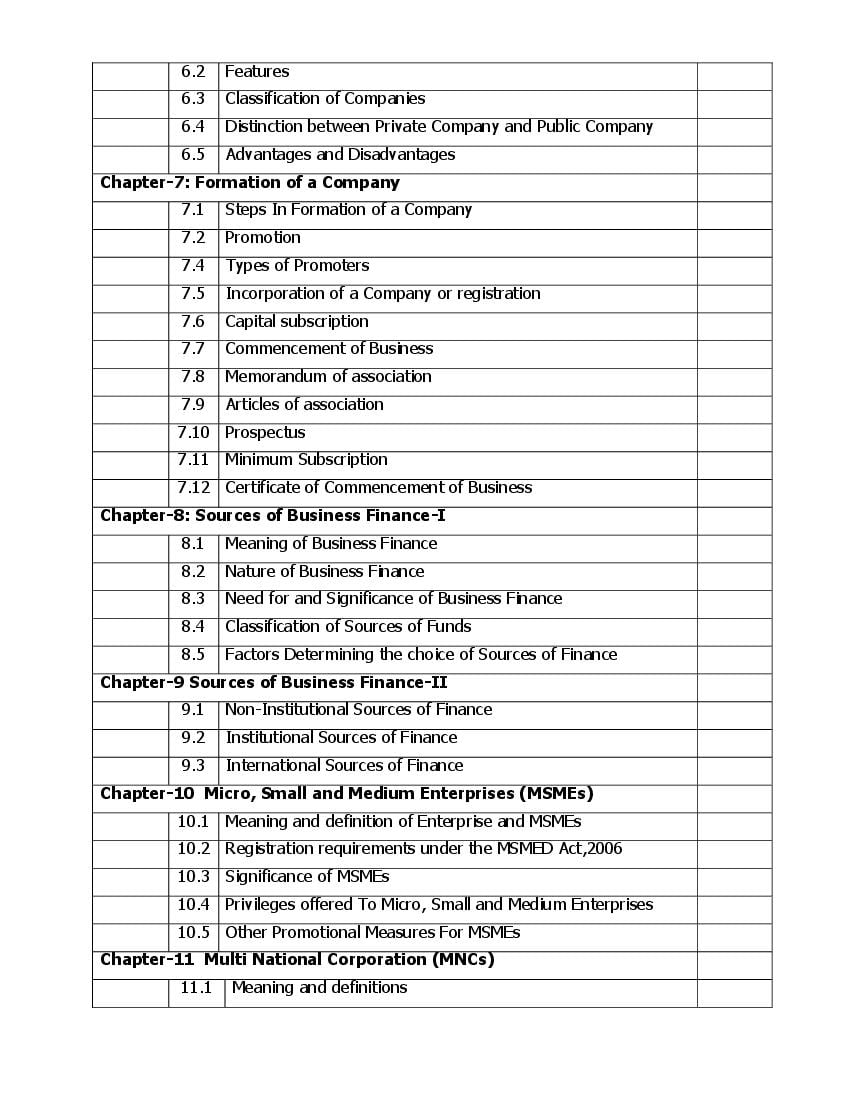

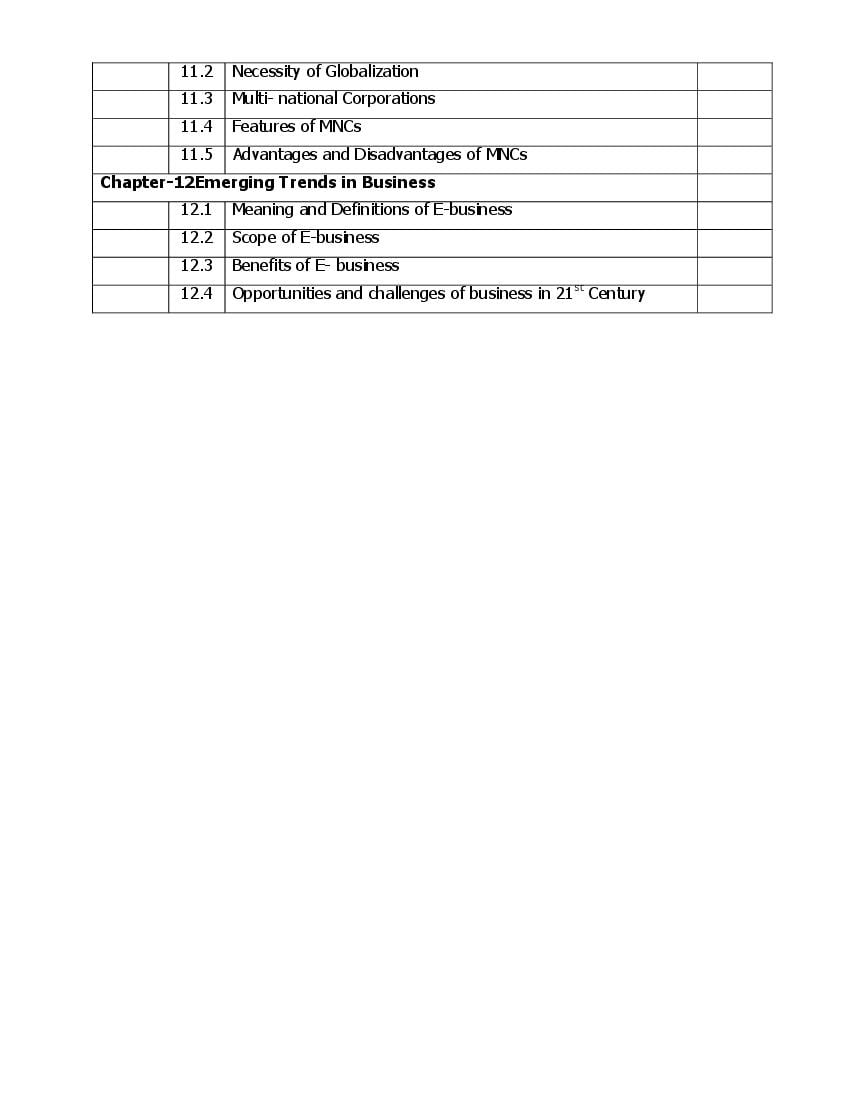

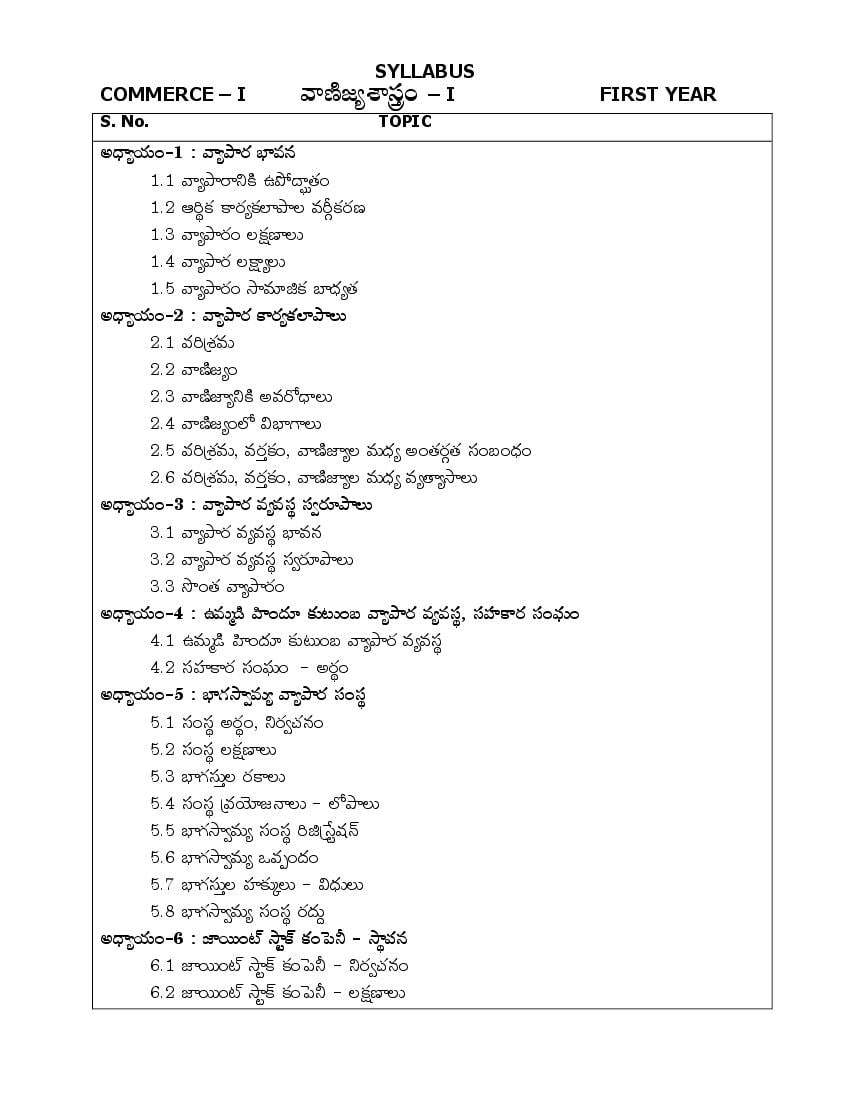

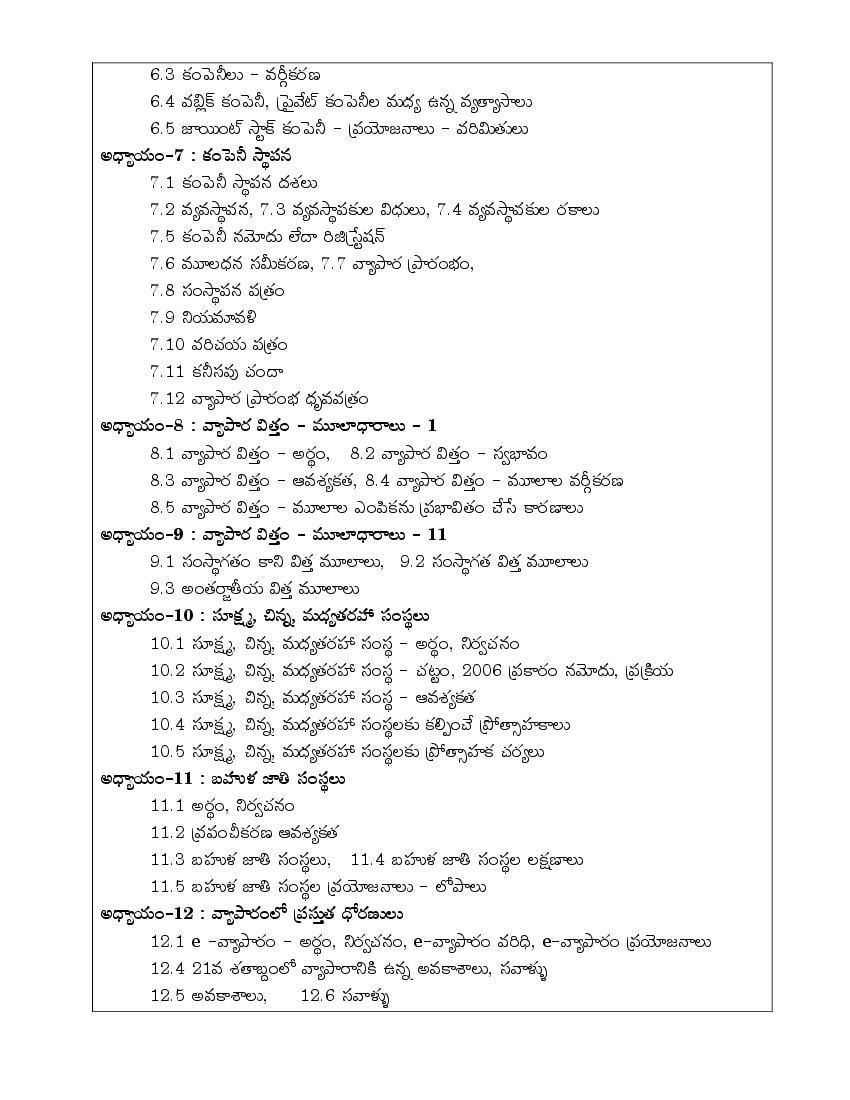

AP Inter 1st Year Syllabus 2023 Commerce View Download

Andhra Pradesh Board Inter 1st Year Syllabus 2024

If you want to know the curriculum for any subject besides Commerce, then you can check all subject-wise syllabus for AP Board Class 11 as follows.

- Accountancy

- Botany

- Chemistry

- Civics

- Commerce

- Economics

- English

- Geography

- Hindi

- History

- Maths IA

- Maths IB

- Physics

- Sanskrit

- Telugu

- Urdu

- Zoology

AP Board Syllabus

And besides Intermediate 1st Year Commerce, you can see all class wise syllabus for Andhra Pradesh board here.

Class 11 Exams

Here are some more resources and details for your Intermediate 1st Year exams.

- AP Inter 1st Year Time Table

- AP Inter 1st Year Results

- AP Inter 1st Year Question Papers

- AP Class 11th Model Paper

Andhra Pradesh Board Inter 1st Year Commerce Syllabus 2024 – An Overview

The key information pertaining to this list of topics is as follows.

| Aspects | Details |

|---|---|

| State | Andhra Pradesh |

| Class | Class 11 / Intermediate 1st Year / Inter 1st Year |

| Subject | Commerce |

| Study Material Here | AP Board Syllabus for Class 11 Commerce |

| More Syllabus of This Class | AP Board Syllabus for Class 11 |

| More Syllabus of This Board | AP Board Syllabus |

| Further Information on This Board | Andhra Pradesh Board |

If you have any queries on AP Intermediate 1st Year Commerce Syllabus 2024, then please ask in comments below.