Tamil Nadu 12th Accountancy Model Question Paper 2026 has been published by DGE TN. You can now download the TN HSC (+2) Accountancy Sample Paper PDF to prepare for your exam. This Tamil Nadu Board Class 12 Model Paper includes specimen questions for the Accountancy subject based on the latest syllabus and blueprint. By practicing with the TN Class 12 Model Paper for Accountancy, you can aim to score full marks in the Tamil Nadu 12th Public Exam 2026.

தமிழ்நாடு போர்டு வகுப்பு 12 Accountancy மாதிரி வினாத்தாள் 2026 உங்கள் 12 ஆம் வகுப்பு போர்டு தேர்வுகளுக்குத் தயாராவதற்கு உதவும் வகையில் வெளியிடப்பட்டுள்ளது. நீங்கள் இப்போது HSC (+2) Accountancy மாதிரி பேப்பர் PDF ஐ இங்கிருந்து aglasem.com இல் பதிவிறக்கம் செய்யலாம். 12 ஆம் வகுப்பின் சமீபத்திய DGE TN பாடத்திட்டத்தின்படி மாதிரித் தாளில் மாதிரி கேள்விகள் உள்ளன Accountancy. எனவே நீங்கள் இந்த வினாத்தாளைத் தீர்த்தால், 12 ஆம் வகுப்பு Accountancy தேர்வில் 100% மதிப்பெண்கள் பெறுவதற்கான வாய்ப்புகளை மேம்படுத்துகிறது.

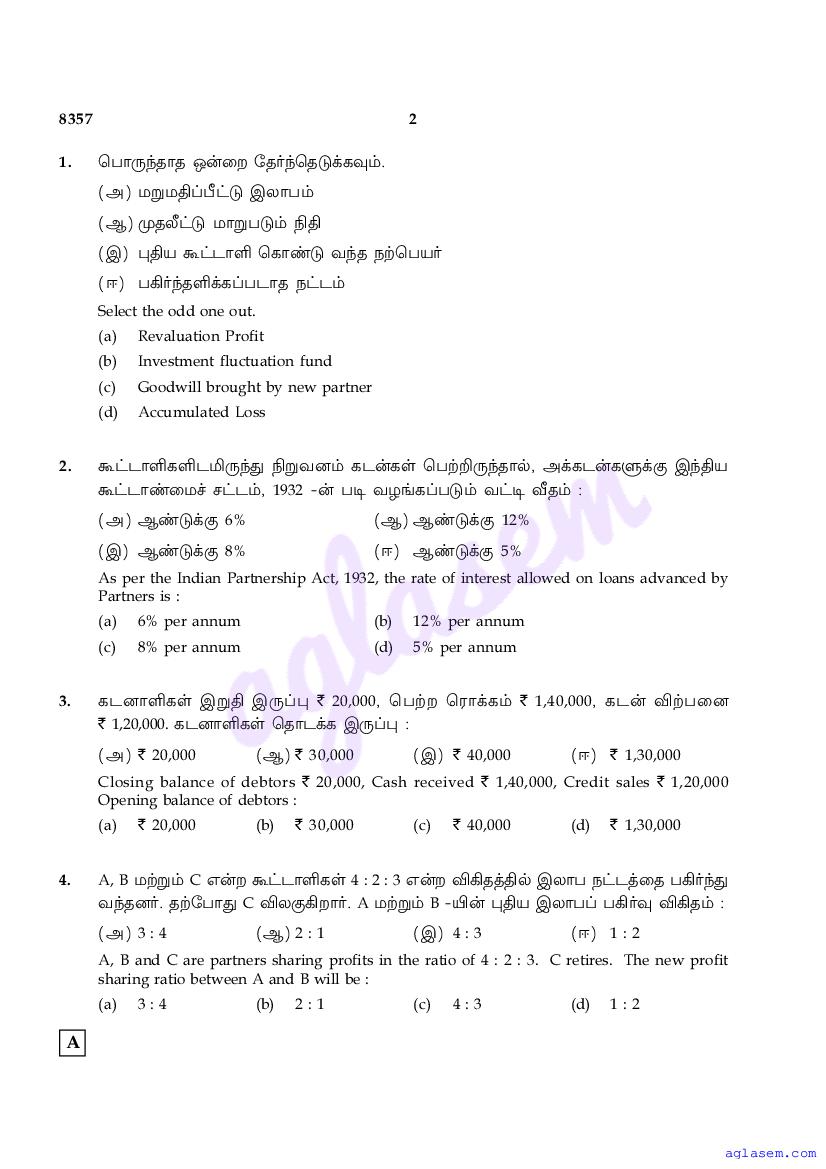

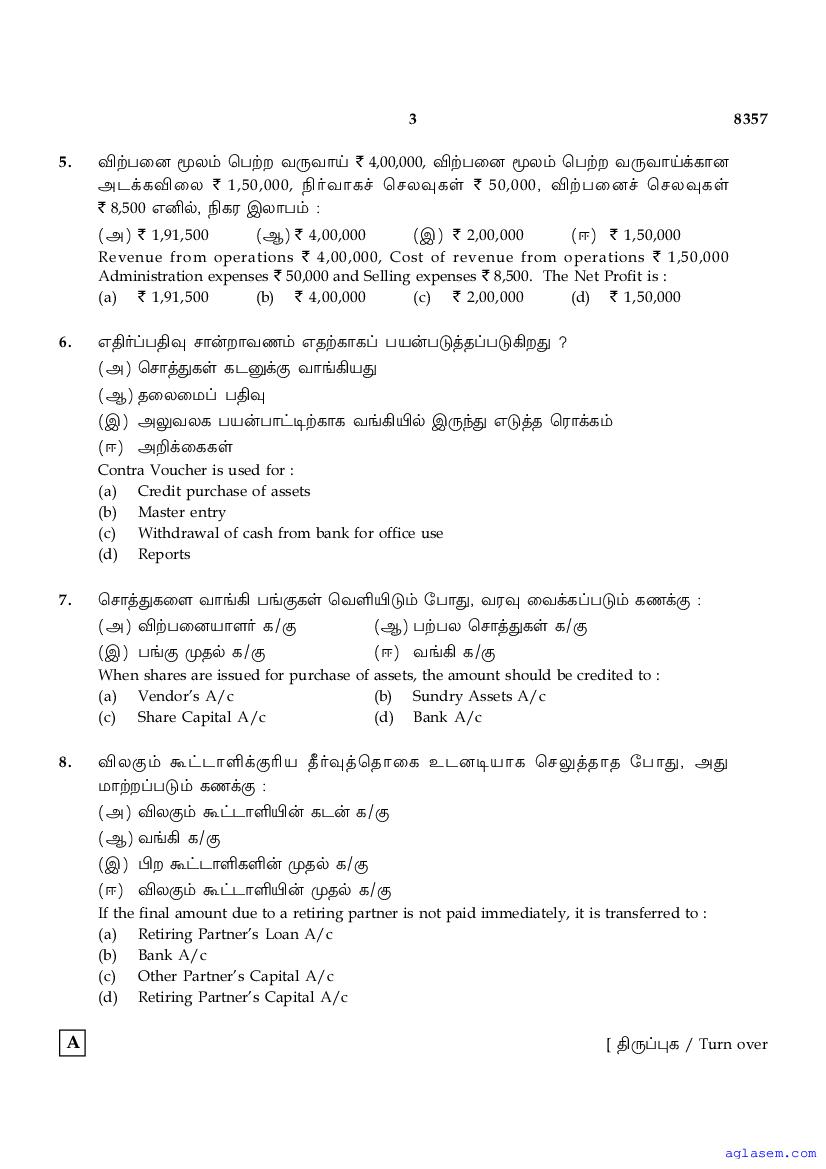

Tamil Nadu 12th Accountancy Model Question Paper 2026

The Tamil Nadu Board Model Paper for class 12 Accountancy is as follows.

Tamil Nadu 12th Accountancy Model Question Paper Download Link – Click Here to Download Question Paper PDF

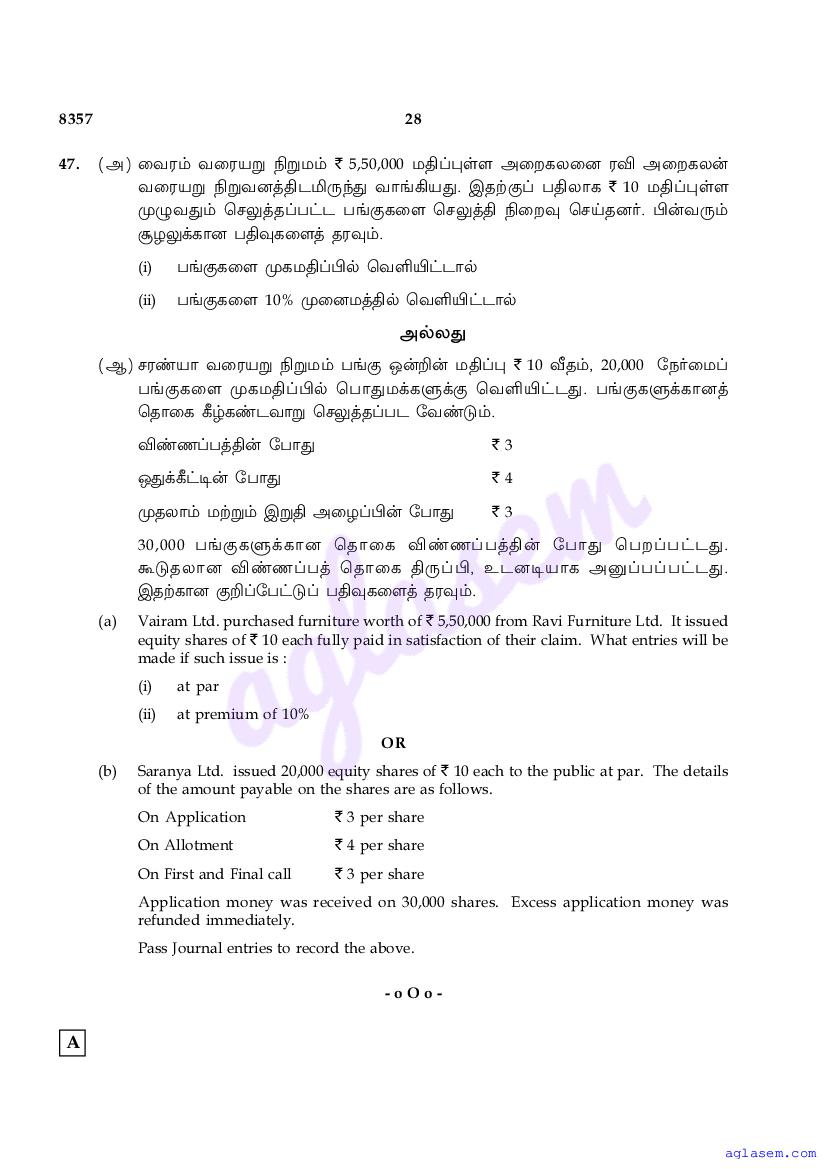

Tamil Nadu 12th Accountancy Model Question Paper 2026 PDF

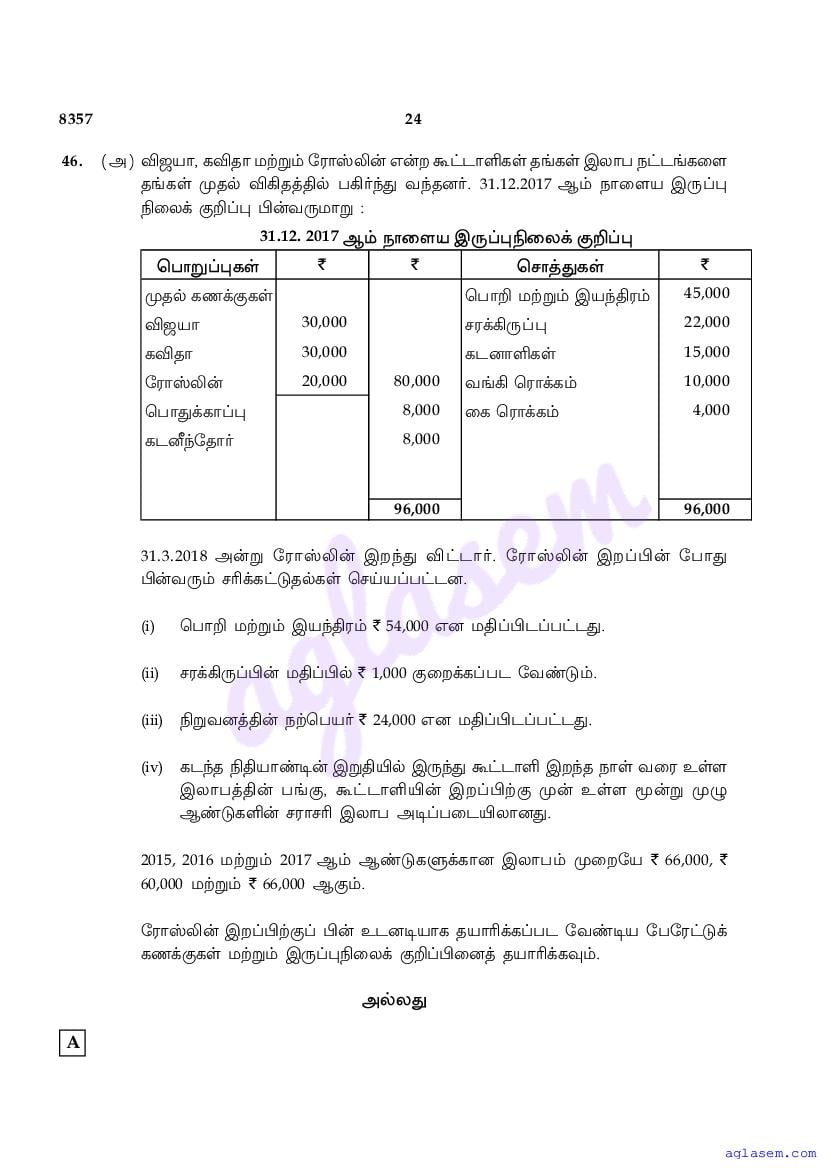

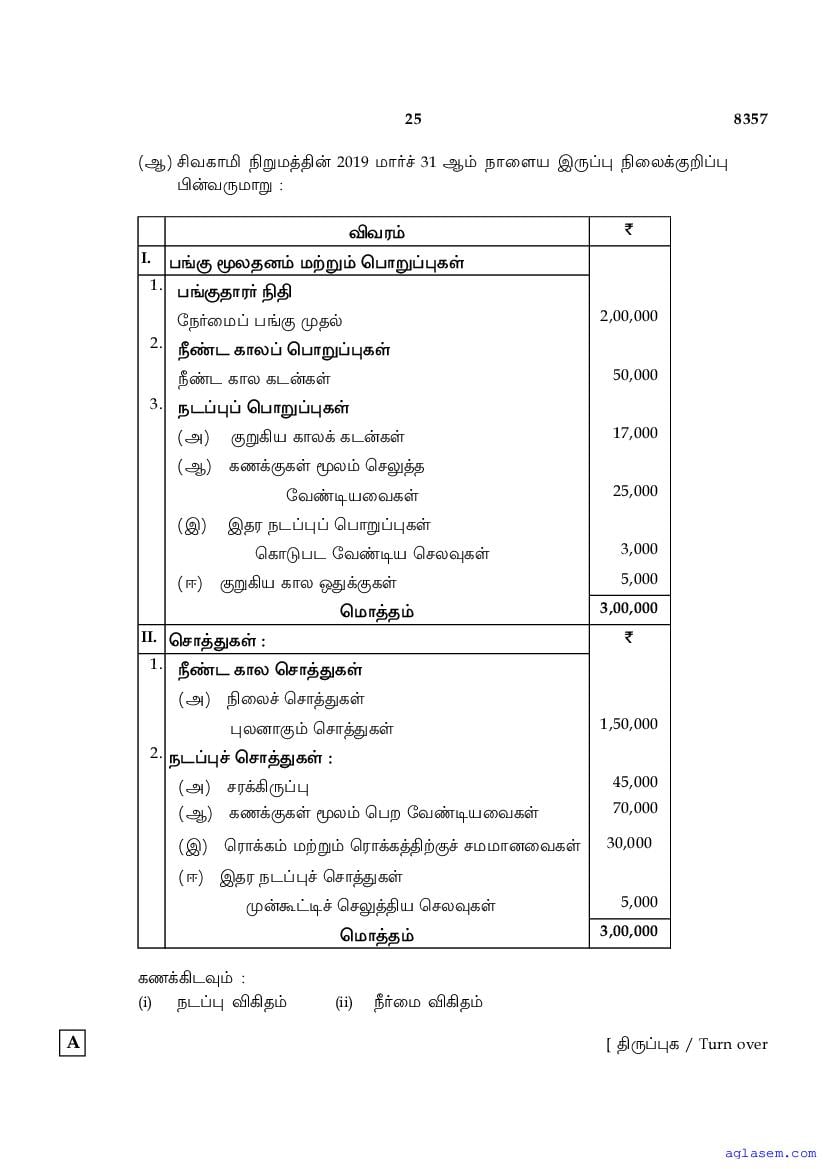

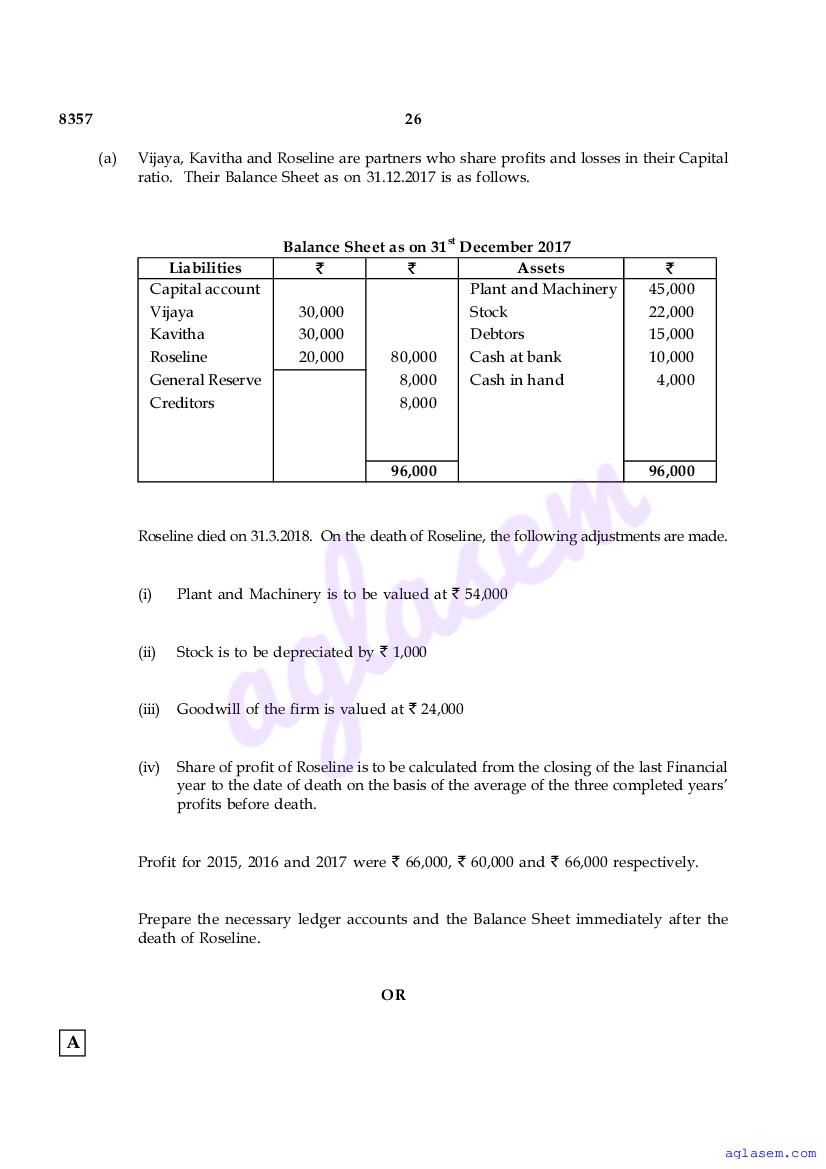

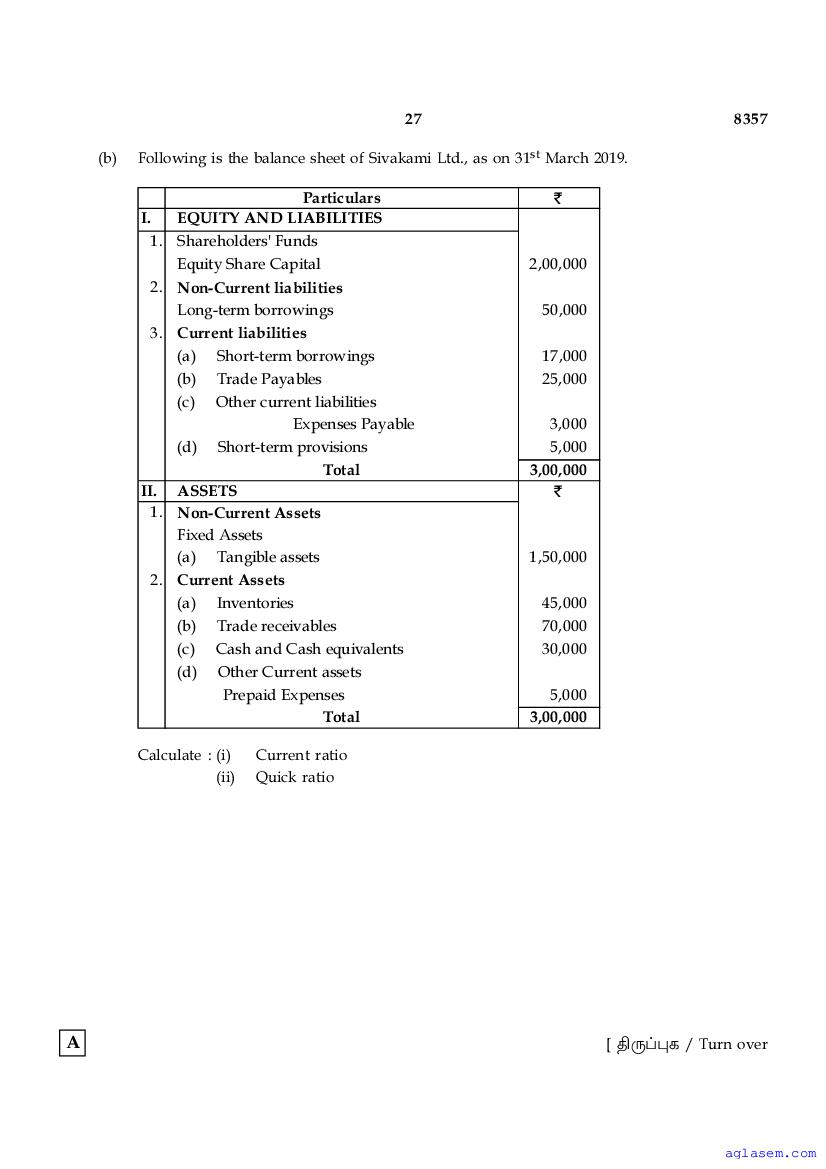

The entire question paper is as follows.

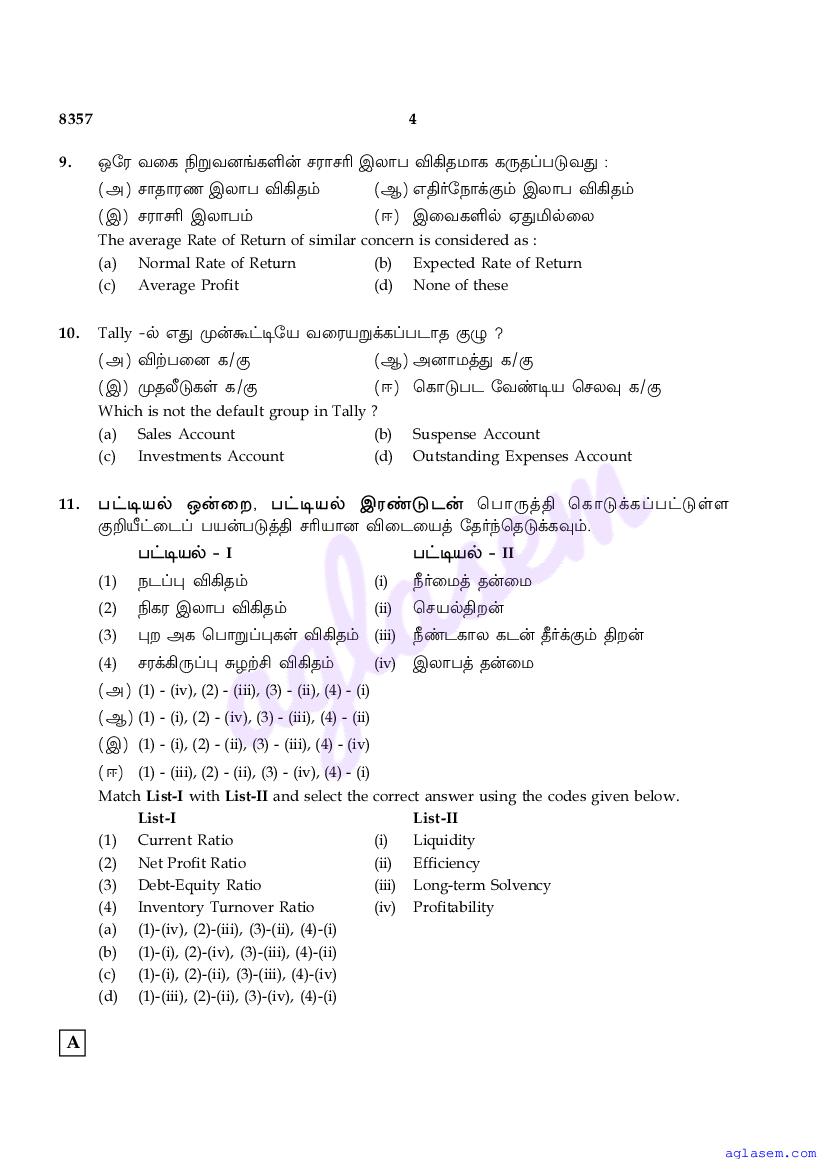

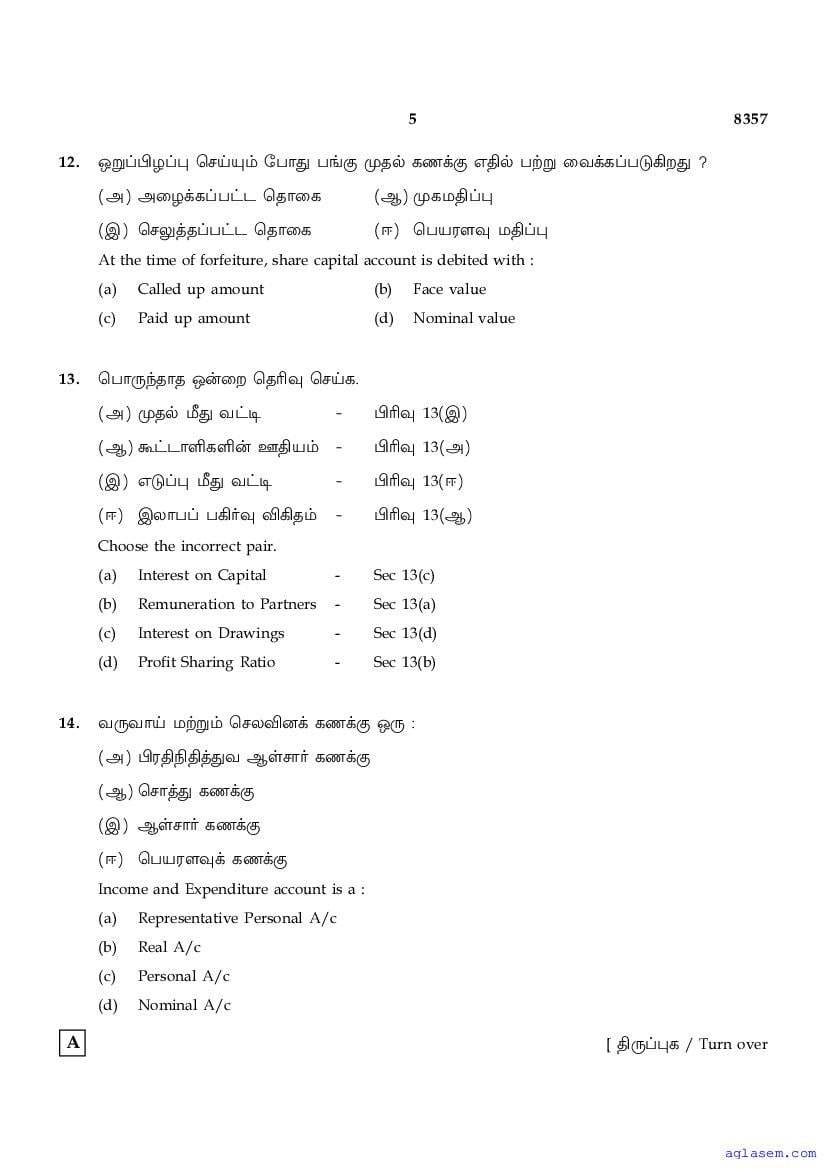

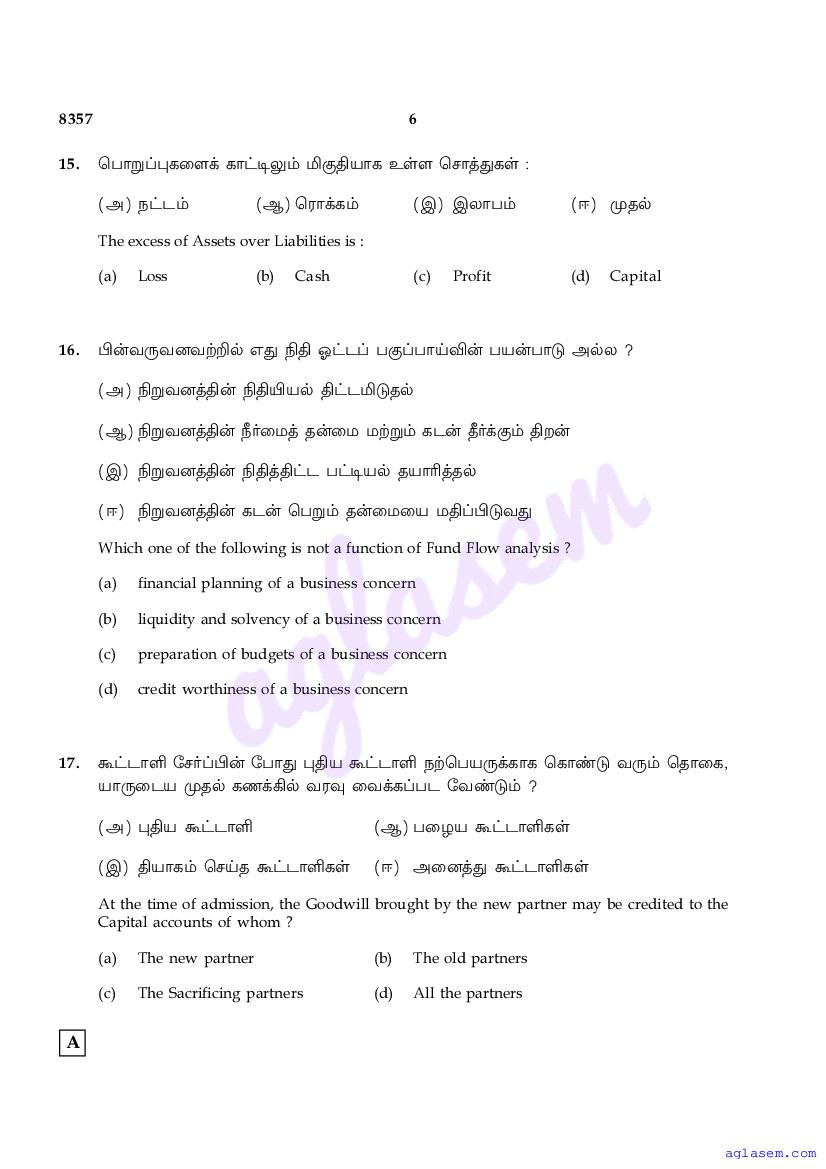

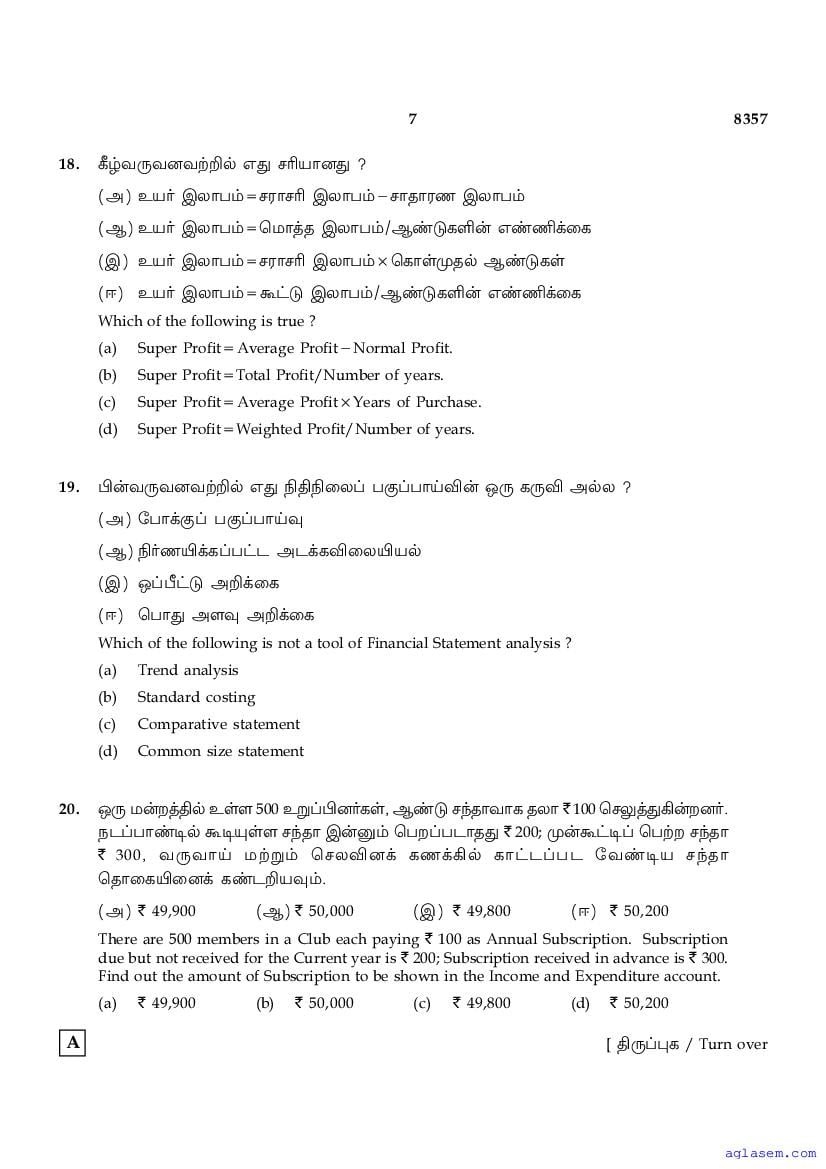

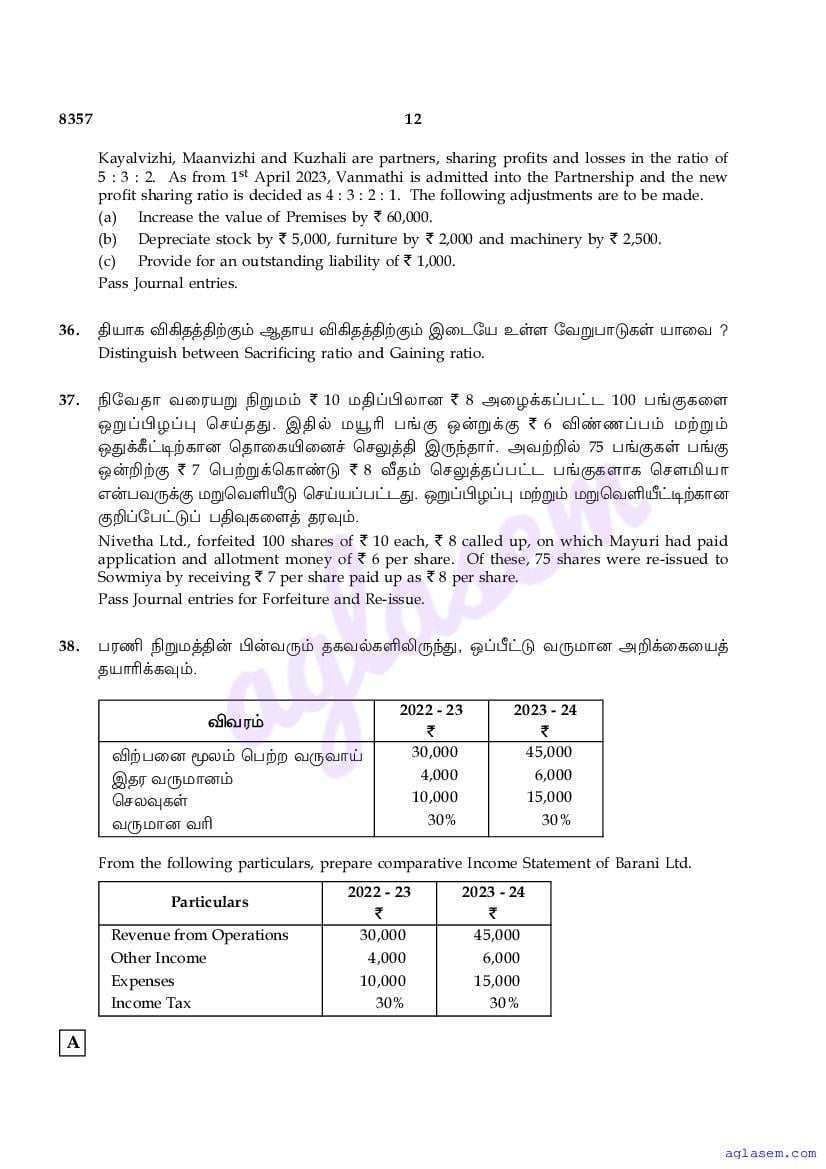

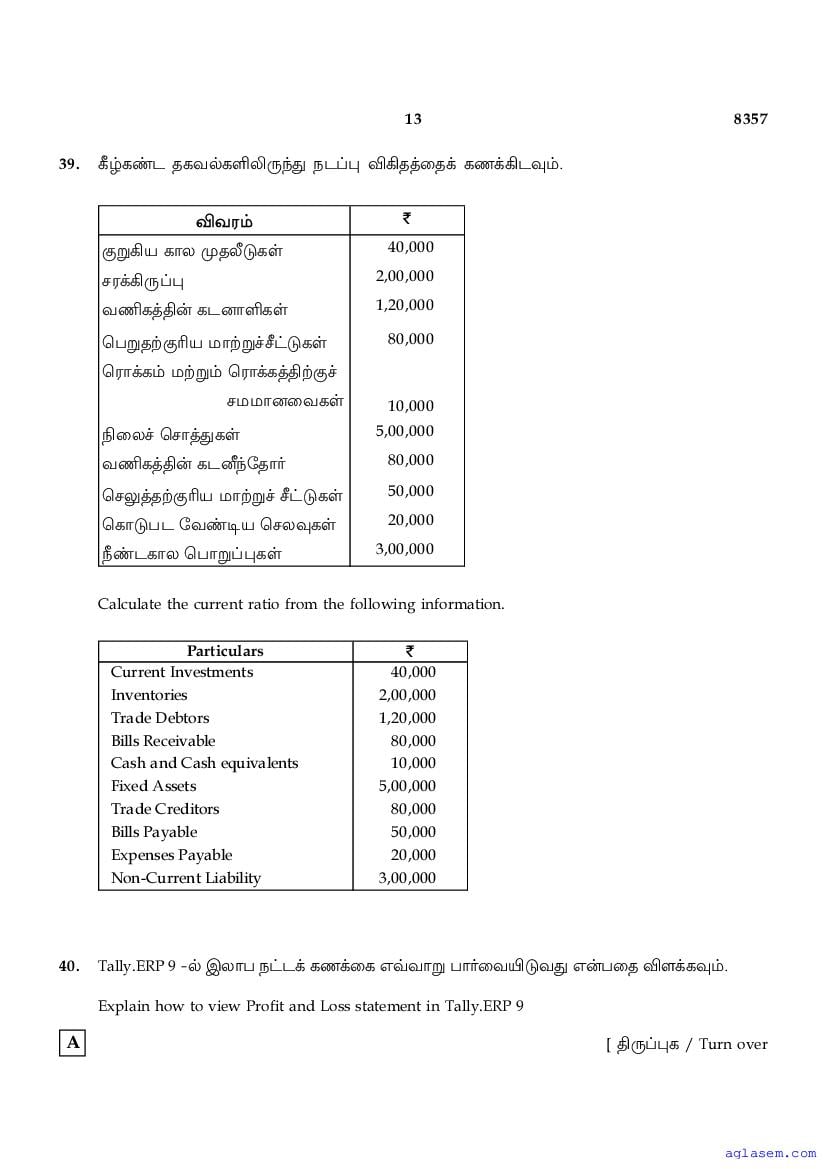

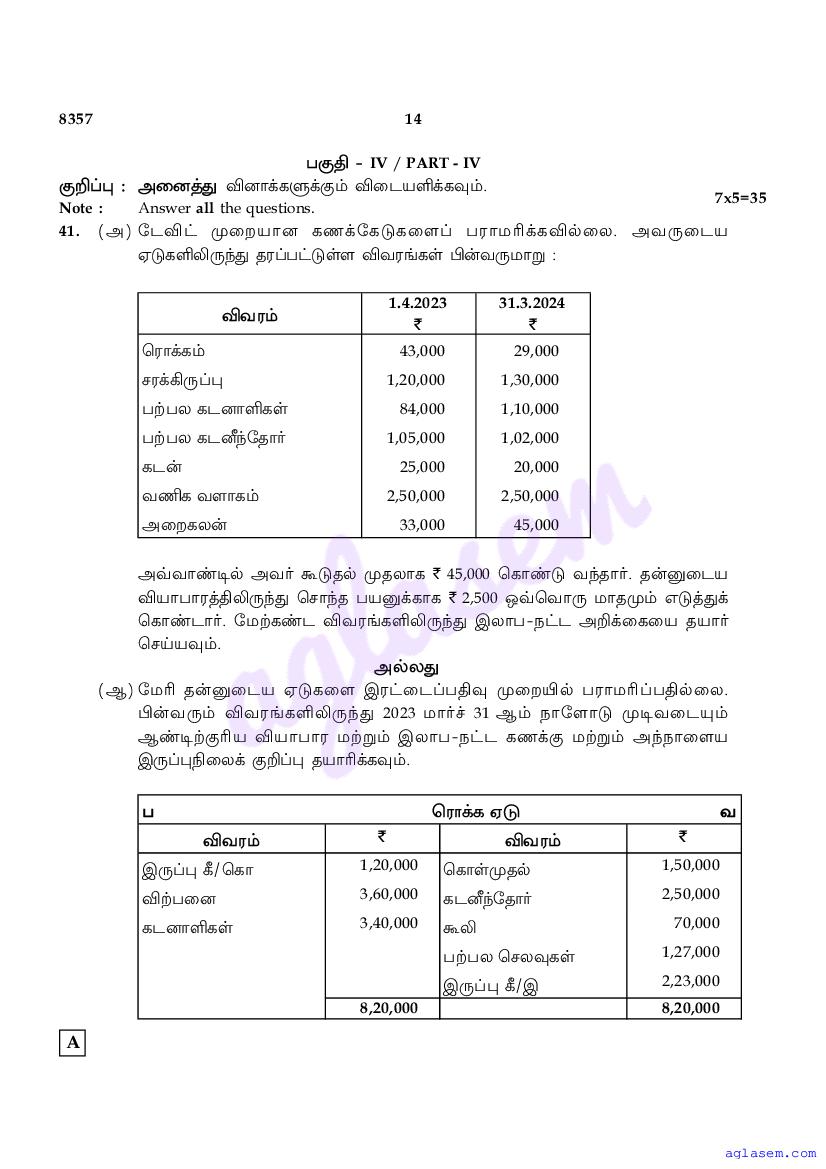

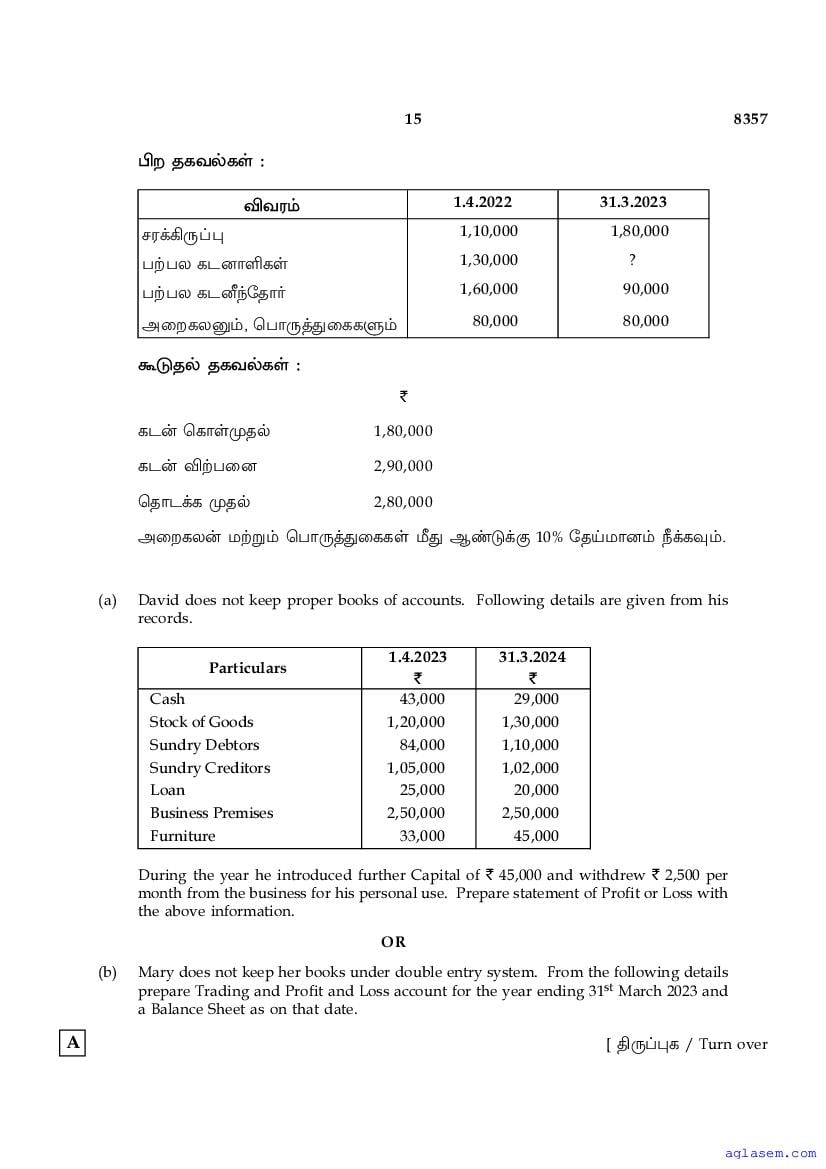

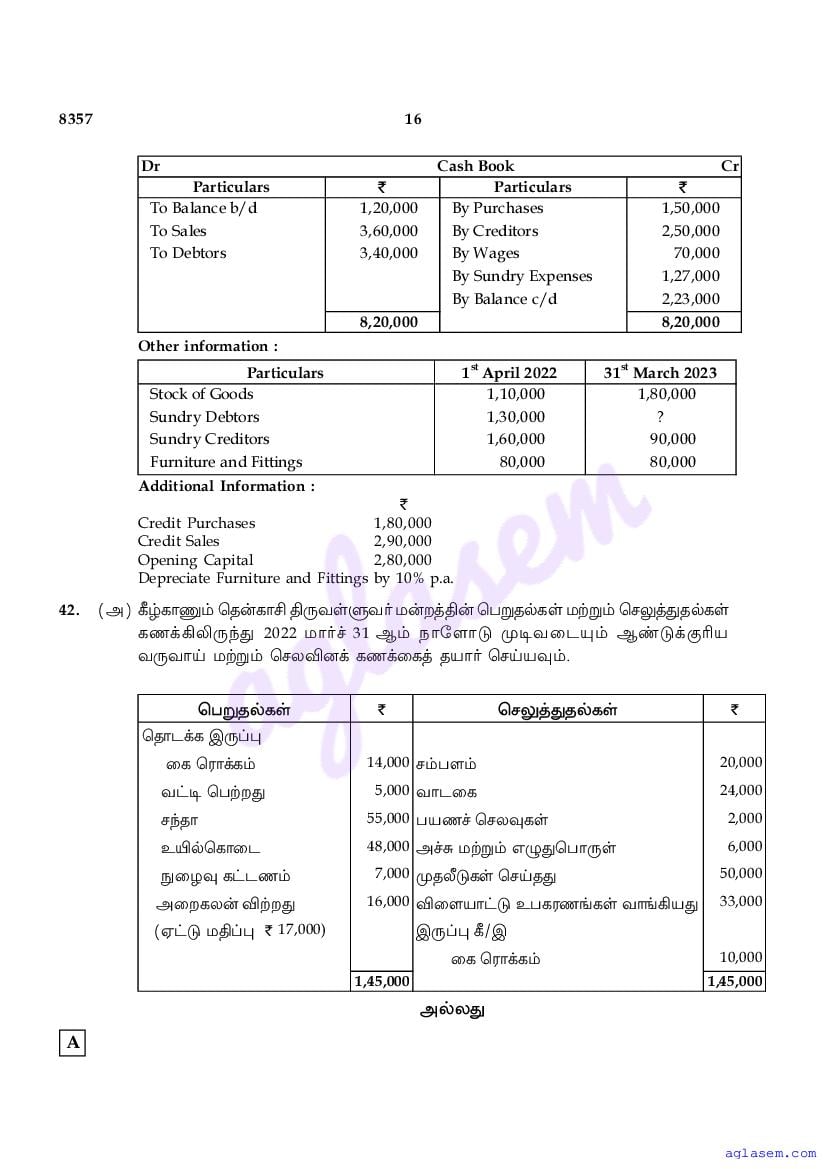

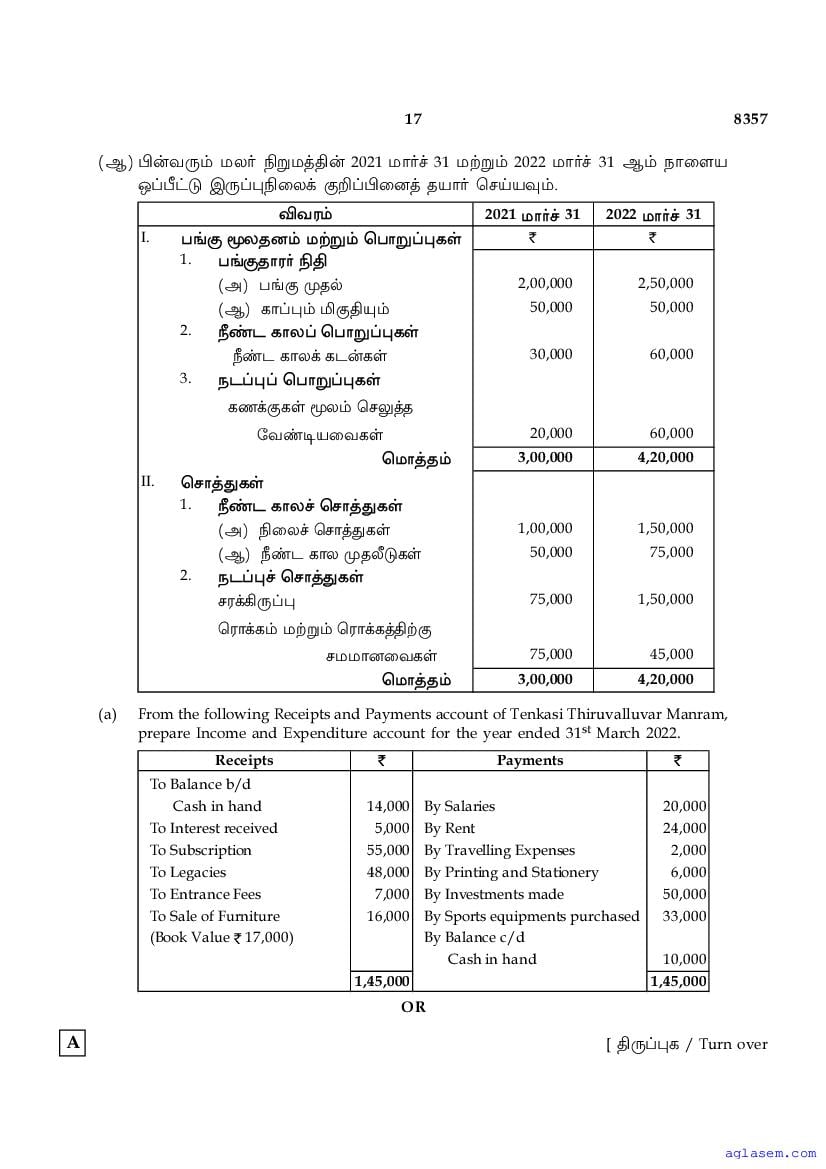

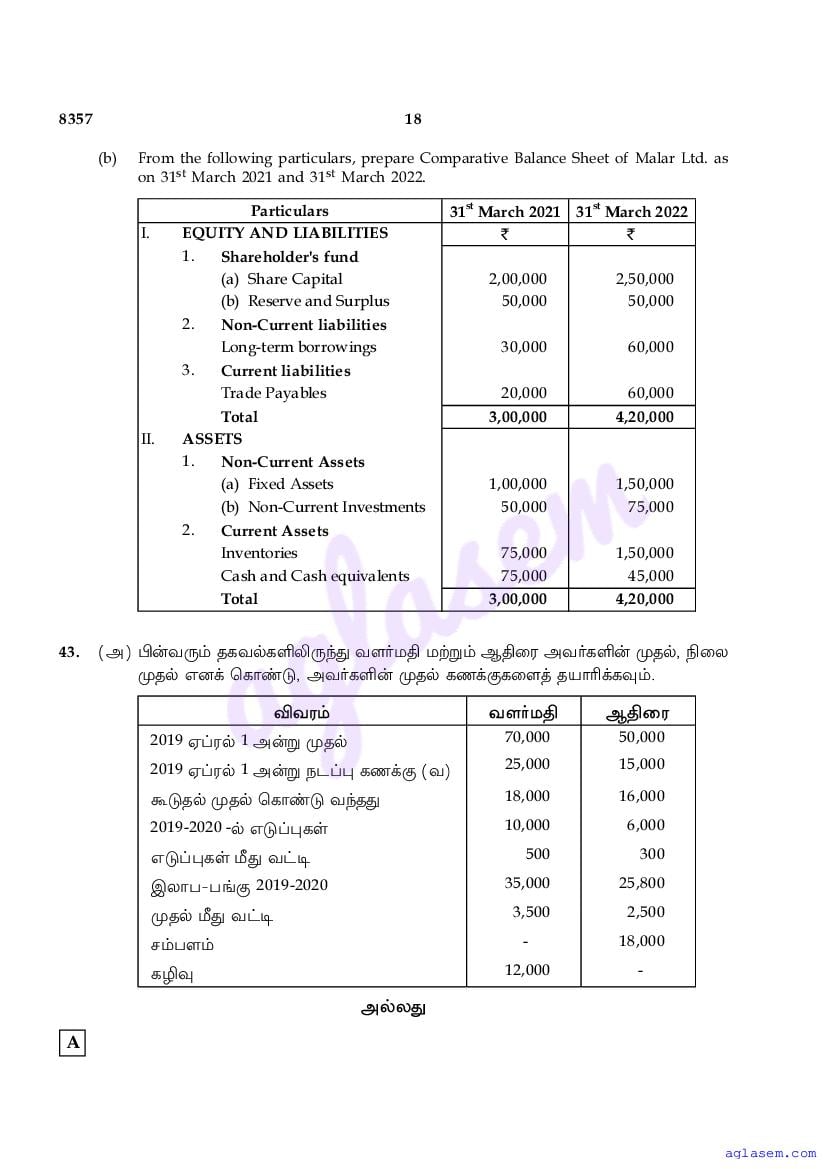

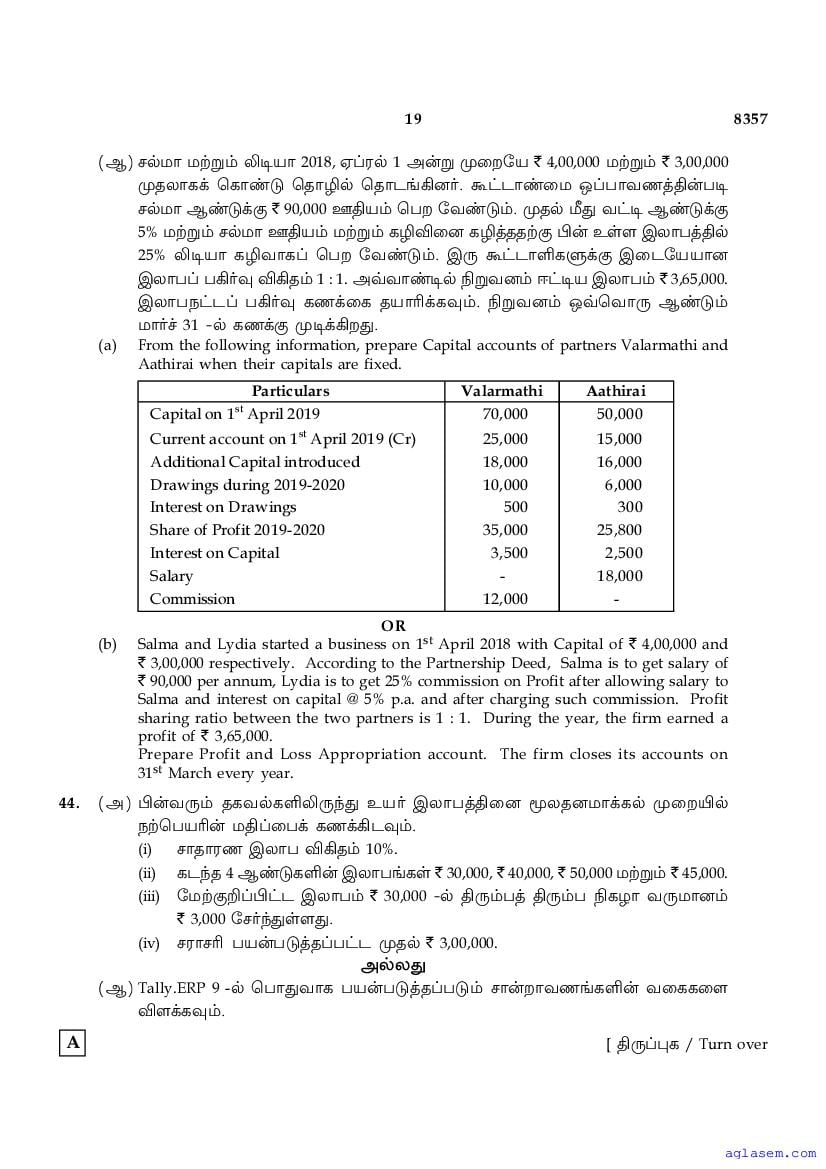

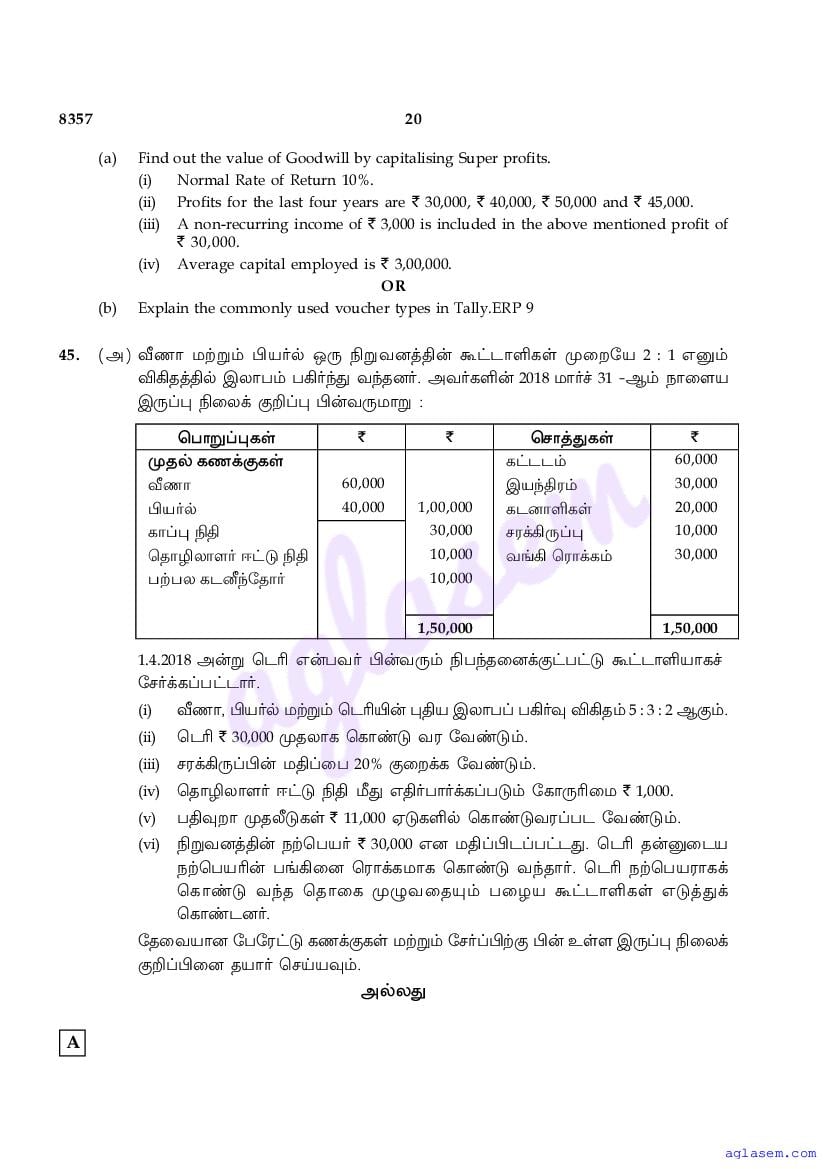

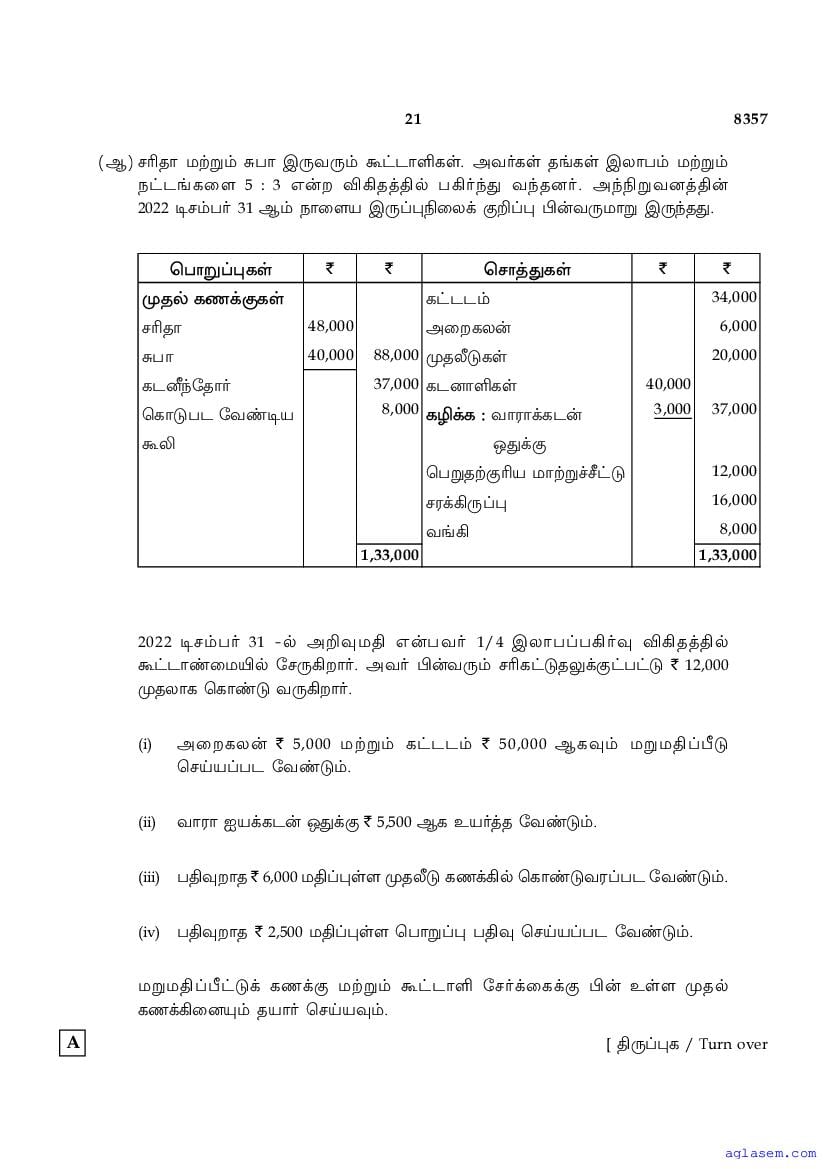

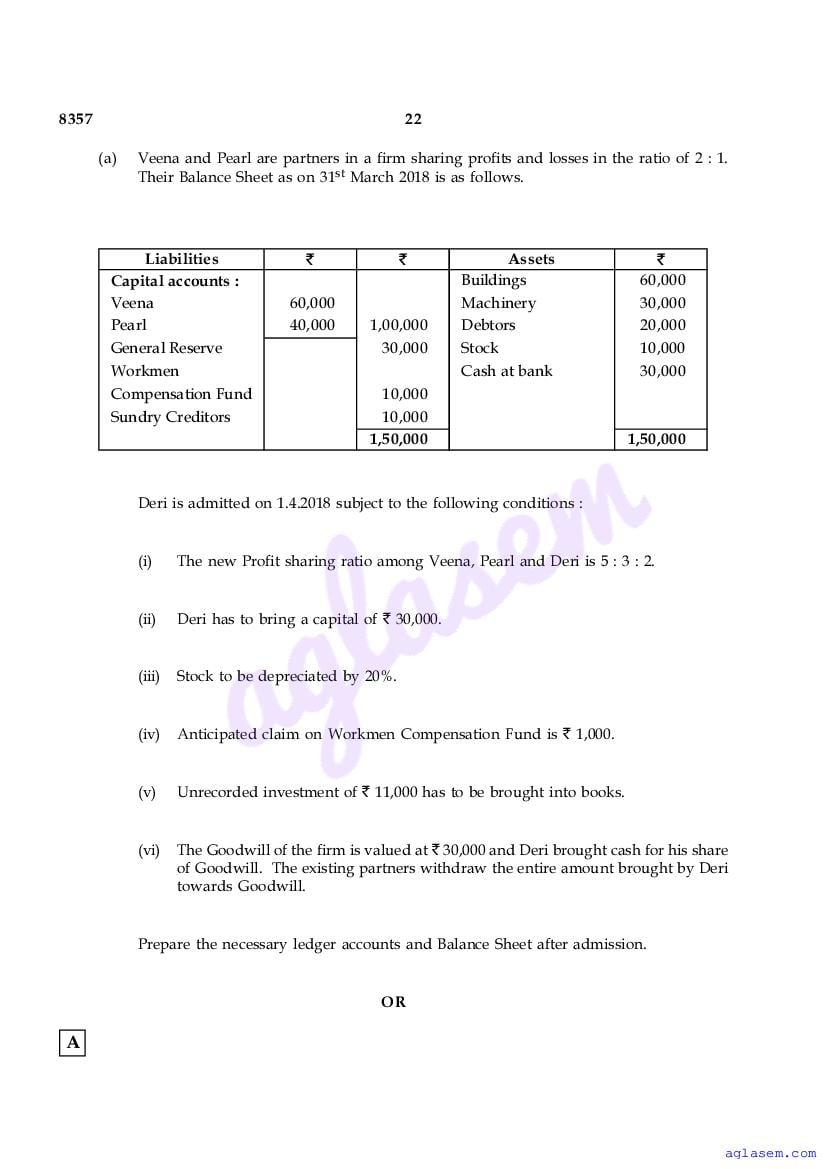

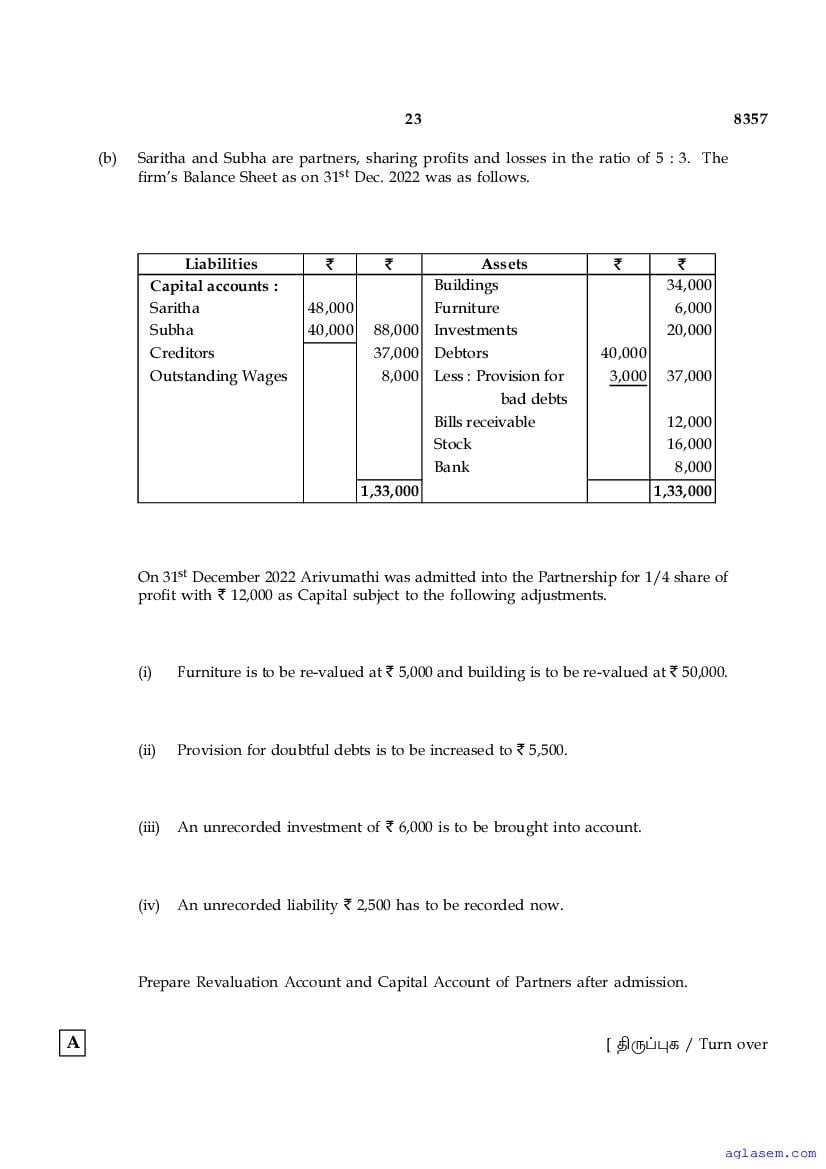

Tamil Nadu 12th Std Model Question Paper 2026 Accountancy View Download

TN Class 12th Model Question Papers 2026

To ace the HSC (+2) exams, you need good marks in subjects besides Accountancy too. Therefore here are all the sample question papers for Tamil Nadu Board class 12.

- Accountancy

- Arabic

- Biochemistry

- Biology

- Botany

- Business Maths

- Chemistry

- Commerce

- Computer Application

- Computer Science

- Economics

- English

- English Communicative

- Ethics & Indian Culture

- French

- Geography

- German

- Hindi

- History

- Home Science

- Kannada

- Malayalam

- Maths

- Microbiology

- Nursing

- Nutrition & Dietetics

- Physics

- Political Science

- Sanskrit

- Statistics

- Tamil

- Telugu

- Urdu

- Zoology

- Vocational Subjects (All)

Tamil Nadu Board Model Papers

The class-wise sample papers for Tamil Nadu board are as follows.

Tamil Nadu 12th Accountancy Model Paper 2026 – An Overview

The key highlights of this study material for Tamil Nadu 12th Public Exam 2026 is as follows.

| Aspects | Details |

|---|---|

| State | Tamil Nadu |

| Class | Class 12 / HSC (+2) |

| Subject | Accountancy |

| Study Material Here | Tamil Nadu Board Model Question Paper for Class 12 Accountancy |

| More Sample Papers for This Class | Tamil Nadu Board Model Question Paper for Class 12 |

| More Sample Papers for This Board | Tamil Nadu Board Model Question Papers |

| Name of Education Board | DGE TN (Directorate of Government Examinations Tamil Nadu) |

| Previous Year Question Papers | Tamil Nadu Board Class 12 Question Papers |

| Exam Dates | Tamil Nadu Board Class 12 Time Table |

| Result | Tamil Nadu Board Class 12 Result |

If you have any queries on Tamil Nadu 12th Accountancy Model Question Paper 2026, then please ask in comments below.

To get study material, exam alerts and news, join our Whatsapp Channel.